May 21, 2026

DACFO Methodology

Read on to learn all there is to know about the DACFO methodology: a structured approach to digital asset accounting, tax, and financial reporting.

Crypto Accounting

Crypto Bookkeeping

Crypto Tax

Digital Assets

A Structured Approach to Digital Asset Accounting, Tax, and Financial Reporting

Most of the time, digital asset accounting is treated as the final step in the reporting process. After all, it is an exercise that begins once all transactions have already taken place.

However, in practice, this framing ensures firms miss where most of their problems actually originate. By the time numbers reach tax filings or financial statements, the underlying issues have already taken root, all due to fragmented data and unclear classifications.

When such foundational elements lack structure, every downstream output begins to drift. That includes tax reports, financial statements, and audit processes.

“The DACFO methodology addresses this problem at its source. Rather than focusing solely on outputs, it establishes a structured, verifiable data framework that aligns with applicable accounting and tax standards from the outset.”

1. Data Completeness and Source Identification

Every collaboration with a client begins with a simple but often underestimated objective: identifying and validating all relevant data sources. In the context of digital assets, this step is rarely straightforward.

Namely, activity is often spread across multiple environments. These include custodial and non-custodial wallets, centralized exchanges, DeFi protocols, staking platforms, and third-party custodians. Naturally, all of them have their own data structures and levels of accessibility.

At this stage, our primary goal is to achieve completeness. After all, even a single missing wallet or overlooked protocol interaction can significantly distort financial outcomes. To mitigate that risk, data collection combines API integrations, raw data exports, and, where necessary, direct blockchain verification. Such a layered approach allows us to ensure the dataset reflects the full scope of activity every time.

Only once completeness is established does the process move forward. Attempting to calculate or classify incomplete data inevitably leads to inconsistencies that compound over time.

2. Transaction Reconstruction and Asset Flow Mapping

With all the data collected, our next step is to transform fragmented transaction histories into a unified and coherent ledger. That is where raw activity typically begins to take on a structure, as we slowly make sense of all the transactions, internal transfers, and asset movements.

Here, the process goes beyond simple aggregation. We take complex transaction flows—such as token wrapping, liquidity provisioning, or multi-step DeFi interactions—and reconstruct them to reflect their full economic substance. Without doing so, we’d have blockchain records that are technically accurate but economically ambiguous.

At this stage, our objective is clarity. By establishing a traceable asset flow, we create a foundation that supports both tax reporting and financial analysis. As a result, it is easier to understand each transaction as a part of a broader financial narrative.

3. Cost Basis Reconstruction and Valuation Framework

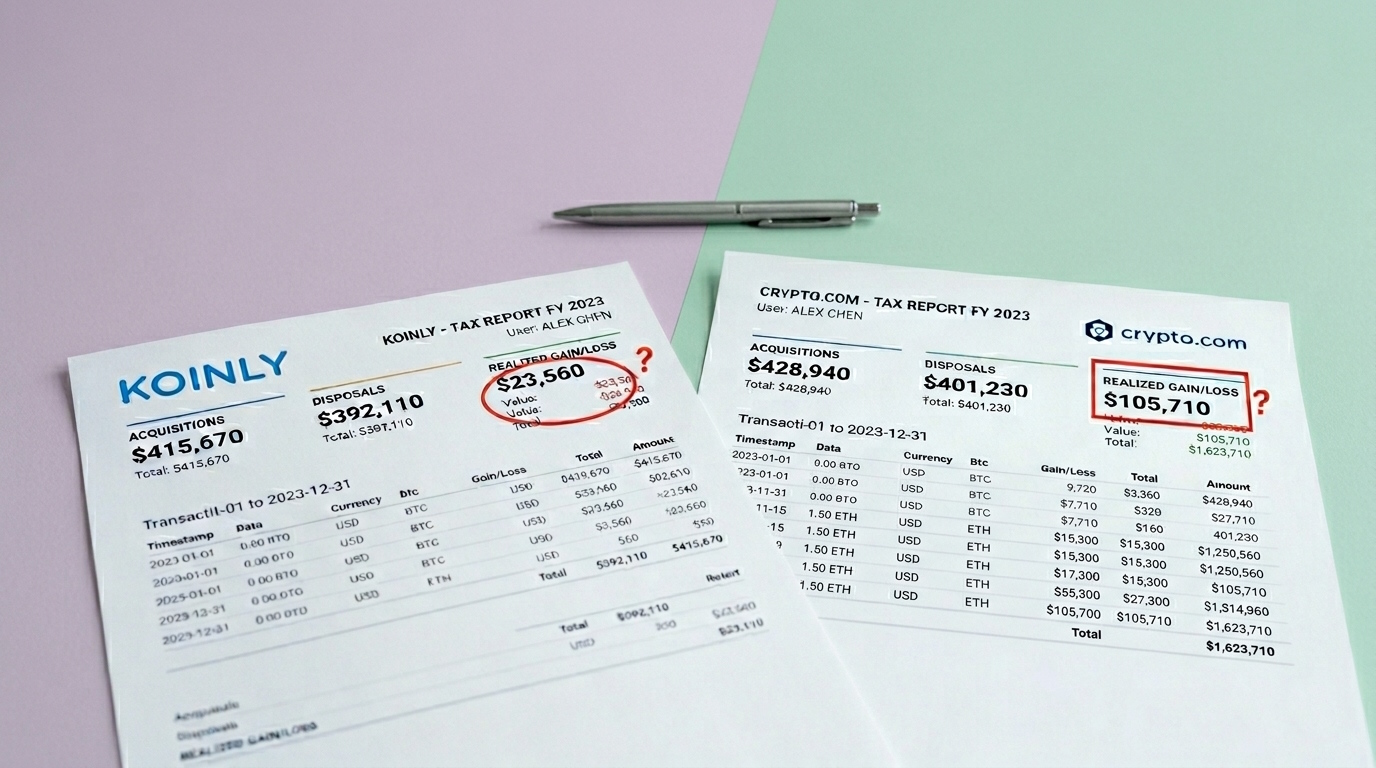

Once we clearly map transaction flows, we can shift our attention to cost abscess and valuation. These elements sit at the core of both tax reporting and financial measurement, yet they are often the first to crack when earlier steps lack structure.

Cost basis reconstruction links acquisition and disposal events and resolves any gaps in historical data. When it isn’t possible to establish direct linkage, we rely on a combination of transaction records, exchange data, and blockchain evidence to establish a reasonable and defensible position.

From a regulatory perspective, this methodology aligns with established frameworks. For U.S. tax reporting, this includes principles under IRC §1012 and related guidance. On the financial reporting side, it reflects the requirements of IFRS—particularly IAS 38 and IAS 2—as well as U.S. GAAP standards such as ASC 350 and the fair value guidance introduced under ASU 2023-08.

As always, consistency remains our defining principle. A uniform valuation approach supported by time-stamped pricing sources and clearly documented assumptions ensures that all assets are measured on a comparable basis across reporting periods.

4. Transaction Classification and Tax Characterization

With valuation in place, we can move on to analyzing and classifying transactions based on their economic substance. This step determines how each activity is treated from a tax perspective. As such, it has a direct impact on both timing and liability.

Transactions typically fall into several broad groups:

- capital events such as acquisitions and disposals

- income-generating activities like staking or mining rewards

- non-taxable movements, including internal transfers.

While these categories may appear straightforward, the underlying classification often requires careful interpretation, particularly in the context of complex DeFi interactions.

The methodology applies relevant tax guidance (such as that issued by the IRS) alongside jurisdiction-specific rules if they are applicable. This fact ensures that classification reflects the regulatory environment in which the business operates.

At this stage, errors tend to propagate quickly. Misclassification can alter the character of income, shift recognition timing, and ultimately distort overall tax exposure. That is why addressing classification with precision is essential to maintaining reporting integrity.

5. Alignment with Reporting Frameworks

Once we have structured, validated, and classified all the data, we can align it with formal reporting frameworks. At this stage, the methodology easily bridges the gap between operational data and regulatory output, ensuring that all reporting draws from a consistent underlying dataset.

For tax reporting in the US context, the necessary steps are transaction-level disclosures on Form 8949, summary reporting on Schedule D, and reconciliation with Form 1099-DA where applicable. For financial reporting, alignment extends to IFRS presentation and measurement standards, as well as U.S. GAAP classification and fair value requirements.

The emphasis is, therefore, on consistency. Financial statements and tax filings should not represent separate interpretations of the same activity. Instead, they ought to reflect a unified view, derived from the same structured data and supported by the same underlying assumptions.

6. Audit Trail and Documentation Framework

As regulatory scrutiny surrounding digital assets continues to increase, the ability to substantiate reported figures has become just as important as the figures themselves. That is why the DACFO methodology incorporates a comprehensive audit trail designed to support both internal review and external examination.

This framework includes detailed wallet-level transaction records, documented cost basis calculations, clearly defined valuation methodologies, and reconciliations between internal data and third-party sources. In addition, it captures evidence of ownership and custody, whether through private key control or custodial confirmations.

Therefore, this stage embeds documentation directly into the reporting process. The result is a reporting environment where every figure is easy to trace and explain.

7. Output and Ongoing Monitoring

The final output is a structured and reconciled dataset that supports multiple use cases simultaneously. In other words, tax filings, financial statement preparation, internal performance tracking, and audit processes all draw from the same foundation.

Where businesses continue to actively operate in digital assets, the methodology extends into ongoing monitoring. In short, we capture, classify, and integrate new transactions into existing frameworks in real time or at defined intervals. That way, we prevent the gradual reintroduction of inconsistencies and ensure that reporting is aligned over time.

To Conclude

Digital asset reporting is so much more than calculations. It depends on complete and validated data, consistent classification, aligned valuation methodologies, and a defensible audit trail—all working together within a single framework.

The DACFO methodology aligns these elements perfectly. By addressing the structural challenges at the data level, it ensures that every downstream output remains accurate and 100% verifiable.

Work With Us

DACFO supports businesses, CFOs, and finance teams in structuring digital asset data and aligning it with applicable tax and accounting frameworks.

If your organization operates across multiple wallets, exchanges, or protocols—or if there is uncertainty around the accuracy of existing reporting—get in touch with us. Together, we can do a structured review and come up with a coherent, scalable framework that will ensure success.

We are waiting for your message!

Read on the topic

Talk to an expert

Book a Consultation